What Professional Women Can Do to Build Pension Wealth

Pension Advice for Women: What Professional Women Can Do to Build Pension Wealth

Perhaps you are a woman who is are starting work, climbing a career ladder, or setting up your own business. Maybe you are leaving work to have a baby, returning work after having a baby, or returning part time. It could be that you are getting close to a milestone age, getting closer to retirement age. Whichever fits your situation, you need to be well-informed about your finances. Specifically, you need to understand the impact of your financial decisions. By taking these actions, you learn how to make the most out of your money. Consequently, this is an excellent way to look after your future self too.

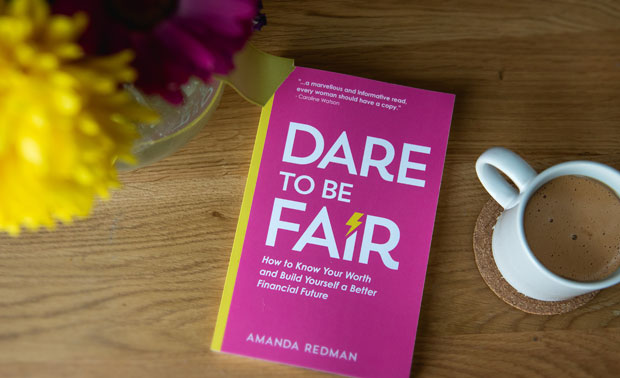

Dare To Be Fair is a new book by Amanda Redman, an award-winning Chartered Financial Planner and pensions expert. Amanda is also a working career mum. The book is a must-read for women of all ages. It encourages them to rethink how they value themselves. At the same time, it acts as a practical guide to help women take control of their finances. In her new book, Amanda reveals the secrets and challenges of financial gender inequalities. She also reveals some home truths about this topic and helps you unlock your financial potential.

Pension Advice for Women & More Money Topics that Dare To Be Fair Covers

The new book covers many topics, including the below:

- Becoming self-sufficient

- Work after children

- Workplace cultures

- Talking to our friends

- How to create a financial plan

- Changing how we view money

- How to fight for fair at work

- Creating a more equal relationship between you and your partner

- Understanding your pension

What can professional women do to build their pension wealth?

Pensions are confusing to many, but that doesn’t mean that you can just ignore them. One of Amanda’s biggest motivations to write Dare To Be Fair was the current pension situation for women. She was motivated by the fact that so many women in their mid-60s are retiring in relative poverty. Or worse, are forced to continue to work because they can’t afford to retire. Women need to take the time and make the effort to understand how pensions work. By doing so, we can take the required action now. Thus, we can avoid not having enough money to see us through the later stages of life.

Firstly, it is never too early to start assessing your pension. Many people are inclined to put off thinking about their retirement finances. They wait until later into their professional career, but starting sooner is better. This will give you a head start. Also, it will provide you with a clearer sense of what you can be worth later in life.

Also don’t worry if you have left it until a later stage in life. Sooner is better but later is better than not at all.

Steps to take control of your finances to build pension wealth

Below, Amanda shares some of her pension tips for women. You’ll find some great tips on what you can do to build your pension pot. Let’s look at three ways you can begin to prepare:

1. Review your current and future finances

Do a self-audit of your incoming and outgoing spend to assess your current finances. Or get together with a loved one or a friend to do this together. You can also do this with a qualified financial adviser if you feel that you need professional input. By reviewing your finances like this, you will gain a clearer picture of your situation. This will help you create realistic financial goals for your retirement.

The above will provide you with valuable insight for two reasons. Firstly, you will know how much you can afford to contribute to your pension regularly now. Secondly, it will let you know what wealth you can expect to accumulate over time. By knowing this, you can decide whether you feel confident that this will be enough for you. Will this plan provide independent financial security in retirement for you? It’s important to plan for unexpected events and ensure you have a buffer to cover them too.

2. Agree ‘fair’ pension contributions with your partner during childcare

For most women, starting a family means having a career break too. This comes with a large reduction in their typical income which can impact pension contributions as well. Contrarily, men don’t typically tend to have the same break from work. Because of this, they are able to accumulate a larger pension pot over the same period.

For that reason, it’s a good idea to agree with your partner about a fair balance of making regular contributions into both of your pensions. Basically, this ensures that both your future finances are being considered, whilst you invest your time into looking after the children. Additionally, if you are not working or earning any income, you can still pay up to £2,880 per year (£3,600 with tax relief) into a pension.

Furthermore, if you choose to not work after having children, you must register for Child Benefit. This is important even if the household earnings exceed the threshold to receive money because simply by registering, if you don’t’ return to work, you will receive a National Insurance credit towards your State Pension for each year until your child is 12.

3. Be smart with how manage your pension

Whilst many people may be content to leave their pension alone, it’s important to understand that there are several ways you can maximise your investment for the purpose of being able to enjoy greater financial comfort in retirement.

Firstly, review any old pensions. If you have several pensions, it can be hard to keep track of them. An experienced financial adviser can help you understand all the options available to you and, most importantly, how they relate to your retirement goals.

Secondly, understand your risk profile and what kind of funds your pension is invested in. If you have a longer timeframe to retirement, it may be appropriate to take a higher investment risk over the next few years. The value of any investment will be directly linked to the performance of the funds you select, and the value can therefore go down as well as up. The result may be that you get back less than you invested. Likewise, the levels and bases of taxation and reliefs from taxation can change at any time and are dependent on individual circumstances.

It’s clear that there is a requirement for better pension advice for women so that they can make informed decisions about their future finances and build pension wealth.

Collaboration.

Related Posts

About The Author

A Mum Reviews

This blog is edited by a mid-30s mum with over 15 years of professional childcare experience. Now 10 years into motherhood and enthusiastic about finding great products and helpful solutions for busy families to make life more fun and easier too.